Stock markets suffer altitude sickness

12 June 2020

Reading the news seems much more complicated these days. Our friend and old colleague, Rob Martorana, has lived and worked in New York all his life. An excellent portfolio manager and great thinker about investments, Rob has written a series of articles for the Chartered Financial Analyst group1 about how to digest news in a way that takes account of its underlying biases. The easy way to do this is to pick a sample from media sources with known biases to judge the central case and the range of interpretations.

The difficulty occurs when those media biases change. This has happened in recent years and particularly recent weeks, with opinions generally becoming more pronounced and polarised. But when events are momentous, those biases can fluctuate and be difficult to judge.

The problem for investors is to try to identify both the biases, and their conscious (and unconscious) swings. It seems to us that, during this pandemic, facts have been sparse but opinions (often dressed up as science) have never been so abundant. The strongest opinions are often about the things people fear – in other words the risks – so risks get amplified and become a ‘fact’ rather than a possibility. This can make markets highly volatile, but also increases the potential reward for being on the other side of those risks.

Financial news reporting also has another problem. Humans want to work out why something is happening. We like cause and effect. As individuals, we gravitate towards those that ‘know’, so when market direction changes, financial journalists feel obliged to identify what looks like the most likely cause and are quick with statements like “the market rose because the US non-farm payrolls were much better than expected”, without it being any more than anybody’s best guess. It may carry some truth at the time, but history tells us there have been many, many occasions when markets have fallen, not risen, after upside surprises in jobs data.

Most professional investors therefore digest financial journalism with a healthy pinch of salt. But it can still be revealing when not taken at face value. The main consumers of the news are active retail investors, and there are times when they can be a significant influence on market direction.

This week has been a case in point, as the rising chorus of financial press commentariat warned how increasingly disconnected lofty stock market valuations appeared against the backdrop of a rather dire medium-term outlook for the economy and relative to historical valuation levels under such circumstances.

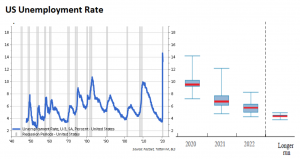

Retail investors have a lot of excess cash for investment just now. In the US, both personal incomes and savings have shot up over recent months, thanks to the various support government measures introduced to bridge the income gap that enforced COVID-19 inactivity has caused (see chart below). This is very different to what usually happens during an economic crisis, but so is the current weekly supplementary payment of $600 for every unemployed adult.

These support measures, along with the stability of the banking system, have prevented the current crisis from becoming a financial catastrophe. This may change towards the autumn, when government support is phased out, but equally could prove a reason for significant optimism if due to diminishing underlying virus issues. Meanwhile, the opening up of the US economy has produced a mechanical bounce in activity. Even if it’s merely progressing from terrible to awful, it feels like a big improvement. Better jobs numbers were inevitable at some point.

Meanwhile, US retail investors can now invest in single shares ‘commission-free’ via Robinhood, a mobile equity trading app. (Of course, free isn’t free. Small investors get a higher price than institutional investors when they buy, and lower when they sell, much like ‘commission-free’ currency exchange at airports). US finance magazine The Reserve Report explains: “it’s really easy to use… with no sports, Robinhood has been filling America’s gambling void. In Q1, Robinhood added 3 million users.” Goldman Sachs is quoted as saying: “By every metric we track, retail activity is the largest since 1999/2000.”

Through May, the flow of retail money into the market began in earnest, picking up the baton from institutional investors. Financial journalists gave investors the positive economy ammunition, even if institutional investors saw the information as not really ‘news’.

Since the beginning of June, however, certain well-known institutional market commentators grew ever louder (initially on social media before being amplified in the financial press) that stock markets were not just getting ahead of themselves, but – more importantly – were anticipating a sharp and steep recovery in corporate earnings which looked far more optimistic than even the most ebullient economists, virologists or epidemologists would have supported. Not overly surprising then that the US market started its 6% sell-off on Thursday after the intervention of a more credible – and even louder forecaster. The US Federal Reserve (Fed) predicted that economic growth would be slow after an initial ‘bounce-back’ surge. The pace of selling quickened sharply after authorities in Houston, Texas said that local coronavirus case rates were increasing and a local lockdown may have to be imposed.

The Fed must be very cautious with its actions and announcements, given how capital markets react to any apparent policy change and how much the real economy is affected by swings in capital market sentiment. Their announcements this week were extremely good news, because they signalled a continuation and duration of liquidity support, which will be much needed to reaccelerate the US economy. Just like the Fed, we do not, and have not for a while, thought that progress towards economic normality would be quick. Even so, there are many reasons to think a return to economic normality might not be as slow as some suggest. Either way, no expert worthy of the title will have the confidence to predict how long it will take for economic normality to return. Even very downbeat projections from the Organisation for Economic Co-operation and Development (OECD) – particularly for the UK – published on Tuesday should be consumed with healthy scepticism about their underlying assumptions. It places emphasis on a ‘second wave’ virus outbreak and assumes lockdown policy responses would be a repeat of the first round. The former may happen, the latter is highly unlikely.

Given what we know about the speculative tendencies of US retail investors, the swift market rebound on Friday leaves us siding with those who suggested that all the above could not be deemed ‘surprises’ to markets. As a consequence, the week’s sell-off was an all-too-natural episode of ‘profit taking’ from some market players, as they experience a significant dose of valuation altitude sickness. At the same time, markets also displayed signs of schizophrenia, given how quickly FOMO returned as Friday’s driver of market sentiment. This ‘fear of missing out’ was prevalent as unusually high valuation levels in markets continue to be reinforced by the distinct lack of alternatives as to where to put one’s surplus cash. As central banks around the world continue to signal that they will keep interest rates and even medium-term bond yields near or below zero, this equates to near certainty of losses of capital or, at the very least, purchasing power for any cash left on deposit or other ‘safe’ assets like government bonds.

The past week has confirmed our expectation that stock and other risk asset markets are likely to see a return of elevated levels of volatility. But over the coming months, markets remain well supported by central bank pledges for open-ended liquidity support. Economic reality will only prevail over monetary liquidity as the dominant market driver once we get a better sense of how long the downturn will last – or (less likely) if governments and central banks withdraw support despite an absence of an end perspective.

In the meantime, our investment portfolio activities will focus on fine-tuning allocations between regions in anticipation of central bank actions, as well as monitoring the progress and sustainability in opening-up economies from East to West. The risk of a second wave of infections continues to linger until such time as more effective treatments – and eventually a reliable vaccine – become available.

Are markets unhappy that the Fed isn’t happy?

In a move that surprised no one, the US Federal Reserve (Fed) announced this week that it will leave interest rates unchanged. The Fed funds rate will remain in the 0-0.25% range, keeping financial conditions easy as the US economy slowly opens up again. To add even more liquidity into the system, the Fed promised to maintain its asset purchase program, buying $80 billion worth of US Treasury bonds a month, as well as $40 billion of mortgage-backed securities. The Fed keeps buying at high levels of volume, but this is nevertheless a slowing of the pace compared to the beginning of the pandemic.

The headline-grabbing news, however, came not from what the Fed did, but what it said. According to the “dot plot” (the graph below showing where Fed members expect interest rates to be over the next few years and beyond) it expects interest rates to remain at near-zero levels until the end of 2022 – an announcement that the media took as a Fed vote of no confidence in the US economy. The Financial Times called it “a dire assessment of US economic prospects” and blamed falling global equity markets on the Fed’s dour outlook. The S&P 500 fell almost 6% by close on Thursday, while both UK and European markets saw daily falls of around 3%. In terms of actual outlook, the Fed expects a 6.5% fall in US GDP this year, but sees activity bouncing back somewhat to 5% growth next year.

In truth, the Fed’s announcement was more realistic than pessimistic, and its forecasts are no different to many being circulated by analysts. The only difference is that the Fed must react to its own expectations, and has therefore decided to keep monetary policy loose until further notice. According to the Fed’s projections, a negative output gap (i.e. the economy runs below capacity) will persist for some time, so low rates will be necessary for as long as this output gap does. Some had expected that soaring asset markets together with a rebounding jobs market might tempt the Fed to ease off the monetary aid ‘life support’. But in his press conference afterwards, Fed Chair Jerome Powell gave no indication that equity or bond markets were presenting any problems, and so policymakers would have had no incentive to remove extensive liquidity support.

As such, we are a little sceptical of how much the Fed’s announcements were the real cause of this week’s wobble in equity markets. There is some circularity in the way market moves and rationales get reported: when markets go up, the press points to some positive news story as justification, then investors pick up on that positivity and buy into markets, causing markets to go up again. Rinse and repeat, with the reverse dynamic occurring when markets fall.

Last week, the positive news came from the better-than-expected change in US employment. Analysts had expected the worst US jobs number on record to worsen further in May, when in actual fact the US economy added 2.5 million new jobs. As we said at the time, this improvement was already being signalled by the high-frequency data – mobility tracking, job listings, credit use, etc. As such, we suspect asset prices had already factored in a fair amount of that positivity.

Throughout the pandemic, liquidity has been the real driver for markets. Capital has flooded into asset markets from central banks (though mostly indirectly) all over the world, pushing up prices beyond what some might consider ‘rational’ given the current economic collapse. The Fed’s main message now is that liquidity is here to stay – even in the face of good news. The central bank’s mission, it seems, is to convince markets – and the public – that monetary policy will remain accommodative until employment is back up to pre-pandemic levels.

To complete that mission, the Fed has to be realistic in its assessment of the economy, and not back down even when capital markets look like they are running hot. As such, up to a point markets should be optimistic: the liquidity fuelling them will be around for much longer to come.

But as Powell stressed, monetary policy cannot do it all. Central banks can flood the financial system with capital, but unless it is being put to work the effect on the real economy will be limited. As we saw in the decade after the global financial crisis, without expansive fiscal policy there is only so much central bankers can do. That is why Powell also used his press conference to point out that government support is still vital. There has been some suggestion that the US spending support packages will wane or stop altogether in the coming months, with politicians not planning negotiations over another COVID-19 stimulus package until late July. But as the Fed Chair rightly pointed out, the more fiscal support the government pledges, the better the results will be.

The Fed’s outlook was not entirely gloomy. Powell pointed out that he expects a full economic recovery over time, with its long-term growth projections still on target. But he did flag the risk of damage to the US’ job creation capacity. Indeed, the Fed’s range projections of unemployment over the next two years vary from not great to historically awful:

That could pose a real problem further down the line. Until now, income and in its wake personal savings rates in the US have improved substantially – as shown in the chart in the lead article. But this is almost entirely due to government support measures. When businesses start making decisions about who to rehire or keep on, that support may drop away – and further economic harm could be in store.

For now, we take heart in the Fed’s commitment to keep markets swimming in liquidity come what may. That is always a positive for assets. Now it is over to the political side.

EM or EU? Where to go when the world opens up

As we wrote last week, the deepening of this global recession has, over the past couple of months, been met with an ongoing rally in equity markets. This growing disconnect may look a little perplexing, but broadly speaking there are two overarching reasons behind it. Ultimately, we know this crisis will pass without totally destroying the global economy. What’s more, governments and central banks are committed to filling the gap with capital in the meantime. These factors have changed the market mindset from ‘should I invest?’ to ‘where should I invest?’ As such, one of the biggest questions facing investment professionals is: Where should I go to make the most of the global recovery?

Regular readers will know that one of our main calls throughout the pandemic has been that emerging markets (EMs) have much to offer. Part of this is conventional wisdom. EMs are pro- cyclical (they do well when global growth is strong, and not so well when it is weak), so any rebound in activity will be of benefit. But given no one knows how deep or protracted the global recession will be, this is not much of a justification on its own. The other element of our EM optimism is China. The world’s second-largest economy was the first hit by coronavirus and the first to start opening up – backed by extensive government and central bank support. China makes up a huge proportion of EM investments (a third of the MSCI EM index is in Chinese assets). And when China whirs into action, wider EMs tend to follow. However, there is now a fly in that ointment.

The recent dramatic heightening of tensions between the US and China over the effective ending of Hong Kong’s autonomy has added a big political risk. That tension is unlikely to abate any time soon, since it comes against a backdrop of high-level disputes and trade tensions stretching back the last four years.

So, where else could offer the same bang for your buck without the political headache? One tentative answer is Europe. While not to the same extent as EMs, exports make up a big portion of Europe’s economy. As such, any rebound in global activity should be a boon for European assets. Things look good on the policy front too. Restrictions are being lifted across the continent, and there is increasingly a drive to get the economy back to work.

Probably the biggest positive is the support coming from both monetary and fiscal policy. We are used to the European Central Bank (ECB) pumping liquidity into the system in times of stress, but the recent announcements of an increase in Eurozone-wide spending (through the European Commission’s new plan), as well as Germany’s long-term fiscal pledges, have been a welcome surprise. ‘Same old problems’ has been the usual crisis response from Europe’s political establishment, but things now look like they are clicking into gear in a strong way.

On both COVID-19 management and the policy response, Europe seems to have the edge over China (and by extension, EMs). While China was the first to start opening up, the pace at which they have done so has been a little disappointing. Now, with European Union countries opening at a faster rate, China’s early advantage has likely already played out. Meanwhile, the ECB is moving full steam ahead with its monetary support, and fiscal measures continue to drip through. In contrast, the Chinese government’s response – though still substantial – has been more cautious than its global peers. Both the government and central bank are less inclined to keep pumping liquidity into the economy, through fears that credit and property bubbles (building in China over the last few years) will return to the surface.

We should not get carried away, however. One of the reasons why European assets have been somewhat neglected by global investors over the last few years is that productivity growth has been poor and there are not many avenues to grow profits. And while fiscal support from EU politicians is a positive, that underlying lethargy has not changed. Deep structural issues remain, which could still be a barrier to any rebound. Moreover, even if Europe can take advantage of a pickup in global growth, the cyclical boost for the European economy is just not as strong as it is for EMs.

But as an investment case, there is a different sense in which Europe has an advantage over EMs – and especially China. Traditionally, the strongest argument in favour of Chinese assets is access to a huge and rapidly growing economy, which continues to modernise and open up to the wider world. But the risk of conflict with the US – whether in trade, technology or even military terms – is a major thorn in its side. Tensions show no sign of letting up – even if the US has a new president come November – and that creates a very difficult environment for Chinese assets.

Europe has its own political problems of course; the threat of a hard Brexit is still very much there and political discontent is widespread. But recent policy announcements have led to some optimism. As such, there is much less political risk in Europe than in China. So, even if growth prospects look better for EMs over the longer term, capital markets might favour Europe over the shorter term – particularly if US-China tensions grow or the ‘risk-on’ sentiment starts to fade.

Much depends on developments from here. Signs of a strong rebound in global activity will favour EMs, but increased US-China tensions will prove damaging. On the other side, further fiscal action will help Europe, while further political stubbornness will hurt them. We will have to watch closely.

Please note:

Data used within the Personal Finance Compass is sourced from Bloomberg/FactSet and is only valid for the publication date of this document. The value of your investments can go down as well as up and you may get back less than you originally invested.